17

Jul

If you’re looking for definition of unbiased estimator pictures information related to the definition of unbiased estimator keyword, you have come to the ideal site. Our site always gives you hints for refferencing the maximum quality video and image content, please kindly surf and locate more enlightening video content and images that fit your interests.

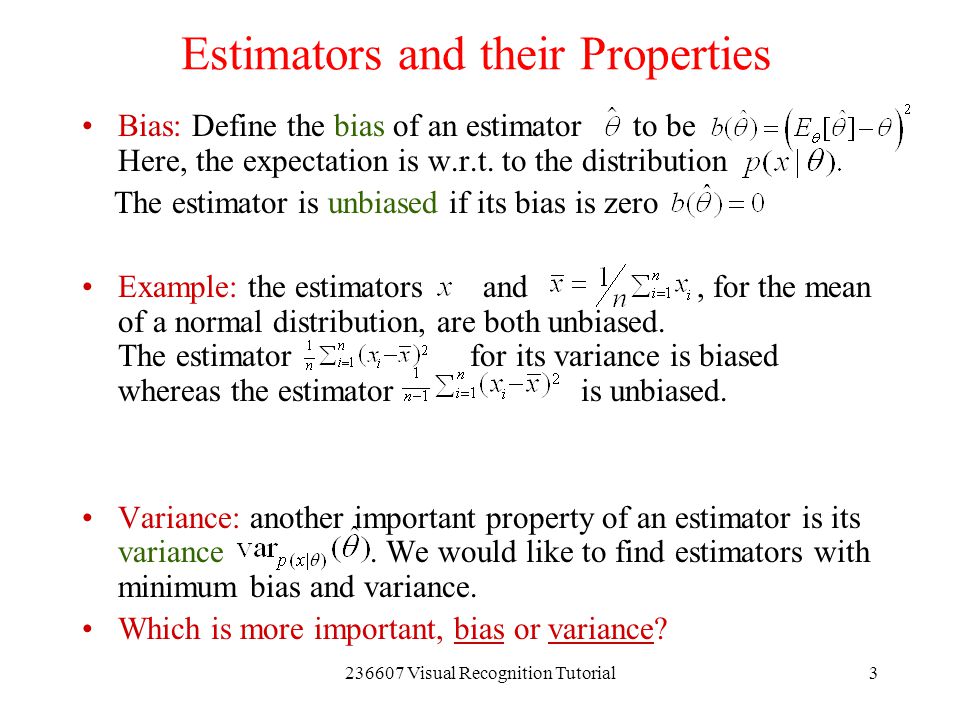

Definition Of Unbiased Estimator. Interpretation of the G-M Theorem. Then the statistic u X 1 X 2 X n is an unbiased estimator of the parameter θ. The unbiased estimator in this case was a negative amount. Finite-sample unbiasedness is one of the desirable properties of good estimators.

An estimator is consistent if as the sample size increases the estimates produced by the estimator converge to the true value of the parameter being estimated. An estimator is finite-sample unbiased when it does not show systemic bias away from the true value θ on average. An estimator is considered to be unbiased if the expected value of the estimator is equal to the population parameter. Interpretation of the G-M Theorem. Any estimator that is not Any estimator that is not unbiased is called biased. Sometimes called a point estimator.

Any estimator that is not Any estimator that is not unbiased is called biased. Interpretation of the G-M Theorem. To be slightly more precise - consistency means that as the sample size increases the sampling distribution of the estimator becomes increasingly concentrated at. An unbiased estimator is a statistic with an expected value that matches its corresponding population parameter. If the population parameter is equivalent to the expected value then the estimator is said to be unbiased. Probability Statistics Unbiased Estimator Variance 1 Comment Estimator.

Previous post

Definition of variable in mathsNext post

Definition of summation notation